Silver's Spectacular Surge: Rewriting Investment Rules in 2025

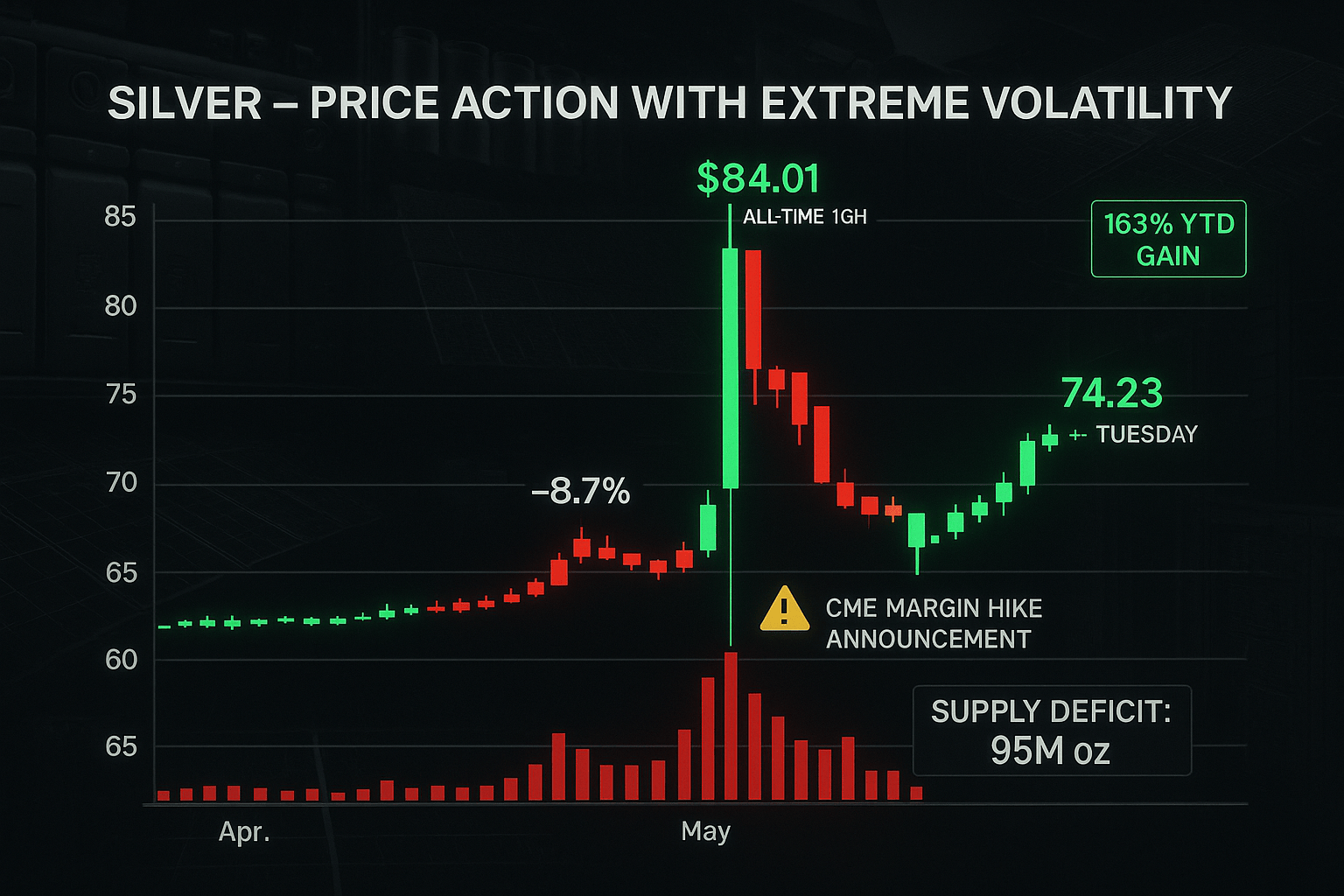

Silver has emerged as the undisputed champion of precious metals in 2024–2025, delivering a jaw-dropping performance that has left investors and analysts scrambling to recalibrate their portfolios. With spot prices soaring to record highs above $66 per ounce in December 2025—representing a staggering 120% year-to-date gain—silver has not only outpaced gold’s impressive 64% rise but has fundamentally altered the investment landscape for precious metals.

This isn't just another commodities rally. Silver’s meteoric ascent reflects a perfect storm of structural deficits, explosive industrial demand, and macroeconomic conditions that have created what many experts are calling a “supercycle” in the making. From Wall Street trading floors to mining boardrooms, the silver story has become impossible to ignore, solidifying its position as a critical asset in the modern economy.

The Industrial Revolution 2.0: Silver’s New Identity

Unlike its precious metal peers, silver has undergone a dramatic transformation from primarily a monetary asset to an indispensable industrial commodity. Industrial applications now account for a remarkable 59% of total silver consumption, with demand reaching a record 680.5 million ounces in 2024—the fourth consecutive annual high. This shift underscores silver's critical role in the accelerating global technological and green energy transitions.

Key Industrial Demand Drivers:

- Solar Energy: The solar photovoltaic (PV) sector is silver’s most dynamic growth driver, consuming 232 million ounces in 2024 and representing 29% of all industrial demand—up from just 11% in 2014. Each solar panel requires 15–20 grams of silver, and with ambitious global targets like the EU's 700 GW solar capacity by 2030, this demand trajectory appears unstoppable.

- Electric Vehicles (EVs): EVs require significantly more silver than traditional vehicles, using 25–50 grams per EV compared to 15–28 grams for internal combustion engines. Automotive silver demand is projected to approach 90 million ounces by 2025, with EVs expected to account for 59% of automotive silver consumption by 2031.

- AI & 5G Infrastructure: The artificial intelligence (AI) boom and 5G rollout have created entirely new demand categories. Data centers—whose global IT power capacity has exploded from 0.93 GW in 2000 to nearly 50 GW in 2025—require silver-intensive hardware. With AI markets growing at 120% year-on-year, this is a demand driver that didn’t exist just five years ago, promising sustained growth.

Investment Landscape: A New Era of Opportunities

The investment ecosystem surrounding silver has evolved dramatically, offering unprecedented access and variety for both institutional and retail investors seeking exposure to this dynamic metal.

ETF Performance Explosion:

Exchange-Traded Funds (ETFs) tracking silver have seen exceptional performance and investor interest:

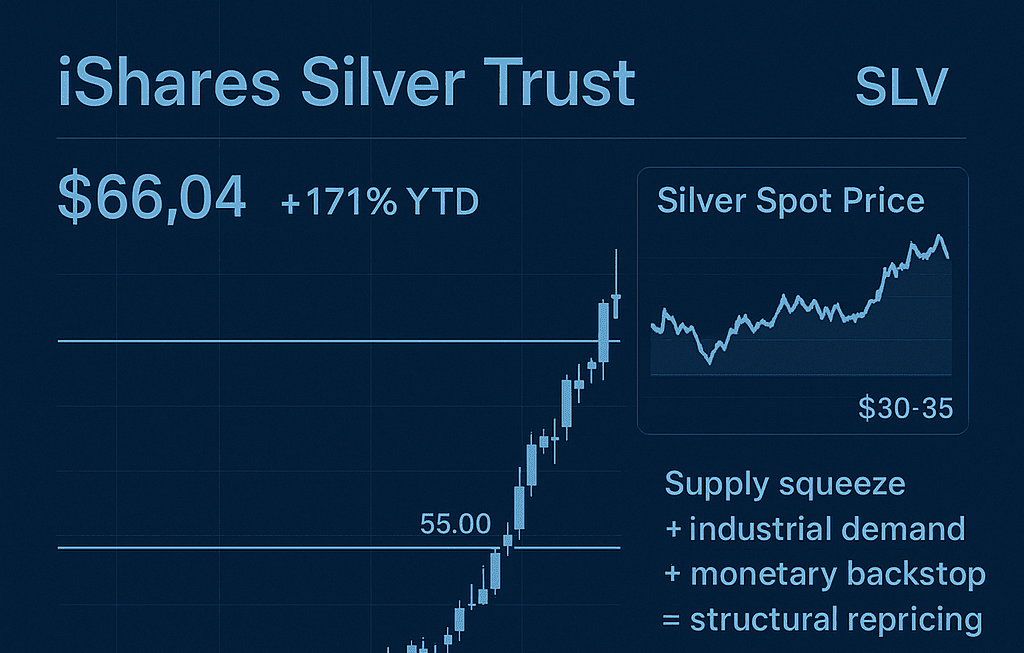

- SLV (iShares Silver Trust): With a 98.01% YTD return in 2025, it's the largest fund, tracking spot prices with high liquidity. It has seen $1.2 billion in net inflows over the past three months.

- SIL (Global X Silver Miners ETF): Delivering a staggering 137.74% YTD return, this ETF offers amplified upside through exposure to silver mining stocks.

- SIVR (Aberdeen Standard Physical Silver Shares ETF): Showing a ~95% YTD return, SIVR is known for its lower fees and direct physical backing.

- PSLV (Sprott Physical Silver Trust): Also with a ~95% YTD return, PSLV provides investors with the option for physical redemption of silver.

Beyond ETFs, silver mining stocks present compelling opportunities. Companies like Vizsla Silver project all-in sustaining costs of just $9.40/oz against spot prices well above $60, highlighting significant profit margins.

Physical Market Dynamics:

The physical market has shown extreme tightness, signaling robust demand:

- London vault withdrawals: A substantial 128.5 million ounces were withdrawn between December 2024 and February 2025, representing a 15.1% drawdown in available supply.

- Lease rates: These have spiked above 11%, with some reports indicating rates as high as 30%, reflecting severe scarcity in the market for physical silver.

Geopolitical Tailwinds and Monetary Policy Support

Silver’s rally has been turbocharged by a convergence of favorable macroeconomic conditions and escalating geopolitical tensions, enhancing its appeal as a safe-haven asset and inflation hedge.

- Federal Reserve: The Fed pivoted to rate cuts in late 2024, reducing the federal funds rate by 100 basis points to 4.25–4.5%. This accommodative stance typically benefits non-yielding precious metals.

- U.S. Dollar: The dollar declined nearly 10% in 2025, its worst performance in eight years. A weaker dollar makes dollar-denominated commodities like silver more attractive to international investors.

- Safe-Haven Demand: Escalating geopolitical tensions in Eastern Europe and the Middle East have driven investors toward safe-haven assets, with silver benefiting alongside gold.

- Sovereign Buying: Notably, Saudi Arabia made its first-ever purchase of silver ETFs, while Russia and India have added physical silver to their strategic reserves, signaling growing institutional confidence.

Analyst Consensus: Bullish Projections and Supply-Demand Imbalance

Leading financial institutions are largely bullish on silver's future, forecasting continued strength. JPMorgan, for example, projects silver to reach $39/oz in 2025 and $56/oz in 2026, anticipating a significant catch-up. Citibank is even more optimistic, forecasting $70/oz for both 2025 and beyond, expecting continued outperformance against gold. HSBC and Macquarie also anticipate strong gains, citing persistent supply deficits and robust Indian demand, respectively, with Heraeus projecting $62/oz driven by safe-haven flows and industrial demand.

This optimism is rooted in a stark supply-demand imbalance. Silver faces its fifth consecutive year of structural supply deficit, with annual supply (~3,100 million oz) falling well short of demand (~4,300 million oz). While mine production is projected to reach a seven-year high of 844 million ounces in 2025, this 2% increase pales in comparison to the explosive growth in industrial consumption.

The Gold-Silver Ratio: A Technical Opportunity

The gold-silver ratio, currently around 92:1, remains well above its historical average of 67:1. This technical indicator signals a compelling opportunity for silver. Historical data shows that when the ratio exceeds 92, silver outperforms gold in 93% of cases over the following year, with median forward returns of 57% for silver versus just 6.8% for gold. This suggests significant room for silver to catch up, further solidifying its investment appeal.

For context, in 2025 YTD, silver has posted a 51.06% return, outperforming platinum (65.02%), palladium (39.74%), and gold (36.36%) when considering its overall performance against major precious metals.

Risk Assessment: Volatility as Both Opportunity and Threat

While the outlook for silver is overwhelmingly positive, investors must be mindful of inherent risks:

- Volatility: Silver is historically 2–3 times more volatile than gold, with an annualized standard deviation near 25%. This presents both significant opportunity for rapid gains and potential for sharp pullbacks.

- Storage & Liquidity: Physical silver requires secure storage and insurance, incurring additional costs and logistical considerations. While ETFs offer instant liquidity, they introduce counterparty risks.

- Demand Destruction: Sustained high prices could potentially reduce demand in traditional sectors like jewelry and silverware. Furthermore, technological improvements in solar panels and electronics aim to reduce silver content per unit, although this is currently offset by sheer volume growth.

Strategic Portfolio Positioning for 2025 and Beyond

For investors looking to capitalize on silver's supercycle, a strategic approach is key:

- Hybrid Approach: A balanced portfolio might include 40–60% physical holdings for wealth preservation and crisis protection, complemented by 30–40% in ETFs for liquidity and tactical trading opportunities.

- Diversification Benefits: Silver offers excellent diversification, exhibiting low correlation with traditional assets (e.g., 0.25 with S&P 500, -0.10 with US Treasuries). Its dual role as an industrial commodity and a safe-haven asset provides unique hedging properties.

The Verdict: Silver’s Supercycle Has Only Just Begun

The convergence of structural supply deficits, explosive industrial demand, supportive monetary policies, and geopolitical uncertainty has created an unparalleled foundation for sustained outperformance in silver. With industrial demand forecast to increase 46% through 2033 and electronics applications expected to grow 55% over the decade, silver’s transformation from monetary metal to technological necessity appears irreversible.

While volatility will undoubtedly remain a characteristic of the silver market, the fundamental drivers suggest this supercycle has significant room to run. For investors seeking exposure to the green energy transition, technological advancement, and a robust hedge against monetary debasement, silver offers a unique and compelling proposition. The question is no longer whether silver will continue its ascent, but rather how high this remarkable rally can ultimately reach.

Key Findings Summary:

- Record Prices: Silver hit over $66/oz in Dec 2025, marking a 120% YTD gain.

- Persistent Supply Deficit: Fifth consecutive year of demand outpacing supply.

- Industrial Demand Surge: 59% of total demand, led by solar, EVs, and AI.

- Bullish Forecasts: Analysts project $39–$70/oz for 2025–2026.

- Risks: High volatility, storage considerations, and potential demand destruction.

- Portfolio Role: Offers diversification, growth potential, and is seen as just getting started in its supercycle.